A War That Could Cost the Arab World $194 Billion

The UN's Most Alarming Economic Report Yet

By @storyrendered · Source: UNDP Assessment, March 31, 2026

Introduction

On March 31, 2026, the United Nations Development Programme published one of the most consequential economic assessments of the year. Titled "Military Escalation in the Middle East: Economic and Social Implications for the Arab States Region," the report strips bare a harsh and urgent reality: a conflict that began on February 28, 2026, now in its fifth week, has already set in motion economic and social damage that could take years — possibly decades — to fully recover from.

The numbers are staggering. Arab economies could collectively lose between $120 billion and $194 billion in GDP. Up to 3.64 million jobs could disappear. Between 3.05 and 3.96 million people could be pushed below the poverty line. And across the region, human development progress equivalent to half a year to a full year could be erased — just like that.

Even a short-lived conflict — one that remains geographically contained — can trigger profound, widespread, and persistent socio-economic damage that ripples across an entire region and beyond. The Arab States region carries deep structural vulnerabilities that amplify even limited shocks into systemic crises.

This article breaks down everything the report covers — in plain language.

What Is This Report and Why Does It Matter?

The UNDP's Arab States assessment is part of a broader series of rapid analyses the organization is publishing on the impacts of the current Middle East escalation. Companion reports are being released simultaneously covering impacts on Iran, Africa, the Asia-Pacific region, and the global development outlook.

The Arab States assessment uses a method called Computable General Equilibrium (CGE) modelling — an economic tool that measures how disruptions in one sector or country ripple through an entire interconnected economy. The report models five escalation scenarios, ranging from a "moderate disruption" (where trade costs increase tenfold) to an "extreme disruption and energy shock" (where trade costs rise a hundredfold and hydrocarbon production halts entirely).

The report covers four sub-regional groupings within the Arab world:

- Gulf Cooperation Council (GCC): Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the UAE

- The Levant: Iraq, Jordan, Lebanon, the State of Palestine, and Syria

- North Africa: Algeria, Egypt, Libya, Morocco, and Tunisia

- Least Developed Arab Countries (LDCs): Sudan and Yemen (Note: Insufficient data prevented modelling for Djibouti and Somalia)

The conflict's transmission channels — the pathways through which a localized war becomes a regional catastrophe — include disrupted trade corridors, volatile energy markets, broken financial flows, and impaired logistics networks. The UNDP describes this as a transformation from "a localized escalation into a systemic regional shock."

The Economic Damage — How Bad Is It?

GDP Losses

The headline figure is devastating. Across the Arab States region as a whole, GDP is projected to decline by 3.7% to 6.0%. In dollar terms, this represents a loss of $120 billion to $194 billion. To put that in perspective: this single conflict, if contained to just four to five weeks, would erase more economic value than the entire region generated in growth throughout 2025.

Projected GDP Losses by Sub-Region (Worst-Case Scenario)

Under the extreme disruption and energy shock scenario

The losses are not distributed equally. Here is how the damage breaks down:

GDP Impact Across Arab Sub-Regions

| Sub-Region | GDP Loss Range | Dollar Equivalent | Primary Driver |

|---|---|---|---|

| GCC (Gulf States) | –5.2% to –8.5% | $103B – $168B | Trade disruption & energy volatility |

| Levant | –5.2% to –8.7% | $17.3B – $28.9B | Conflict proximity & supply chains |

| North Africa | 0.0% to +0.4% | +$0.09B – +$3.2B | Relative insulation (marginal buffer) |

| LDCs (Sudan & Yemen) | –0.1% to –0.5% | $70M – $320M | Fragile economies, outsized human cost |

The GCC and the Levant together bear the overwhelming share of the economic burden. The UNDP attributes this to their structural exposure — the GCC because of its deep integration with global energy markets, and the Levant because of its geographic proximity to the conflict and its already-fragile economic baseline.

What Is Driving These Losses?

The report identifies three primary transmission channels through which the conflict is causing economic damage:

1. Increased trade costs. Even moderate disruptions drive up the price of moving goods. Insurance premiums for cargo ships spike. Shipping routes lengthen or close entirely. Businesses face unpredictable delays and cost overruns.

2. Temporary productivity losses. Businesses reduce operations or close. Workforces are displaced. Agricultural cycles are interrupted. Tourism — a major revenue source for countries like Egypt, Jordan, and Lebanon — collapses.

3. Localized capital destruction. In conflict zones, physical infrastructure — factories, ports, power stations, roads — is damaged or destroyed, removing productive capacity from the economy for years, sometimes permanently.

Jobs — 1.61 to 3.64 Million Lost

The employment impact of this escalation is catastrophic in its scope. Across the Arab States region, unemployment is projected to rise by 1.8 to 4.0 percentage points — translating into between 1.61 million and 3.64 million jobs lost.

Those 3.64 million jobs at the upper end represent more than the total number of jobs created across the entire region in all of 2025. An entire year's worth of employment progress, wiped out in weeks.

Jobs Lost by Sub-Region (Upper Estimate)

Millions of positions eliminated across all sectors

Employment Impact by Sub-Region

| Sub-Region | Unemployment Rise | Jobs Lost | Key Sectors Hit |

|---|---|---|---|

| GCC | +3.6% to +9.4pp | 1.17M – 3.11M | Oil & gas, aviation, hospitality, finance, construction |

| Levant | +2.3% to +2.7pp | ~320,000 | Compounded by pre-existing high unemployment |

| North Africa | ~+0.1pp | ~60,000 | Moderate impact relative to other sub-regions |

| LDCs (Sudan & Yemen) | +0.2% to +0.8pp | 50K – 200K | Economies with almost no safety nets |

The GCC's disproportionate job loss figure — up to 3.11 million — reflects its large expatriate workforce and the sectors most exposed to geopolitical volatility: oil and gas operations, aviation, hospitality, financial services, and construction. These industries are not just economically significant; they are the employment backbone of the Gulf.

Poverty — 3.05 to 3.96 Million Pushed Below the Line

Of all the statistics in this report, the poverty figures may be the most morally urgent.

Across the Arab States region, the escalation is expected to push between 3.05 million and 3.96 million additional people into poverty. The regional poverty rate is projected to increase by 0.70% to 1.00%.

But the distribution of this suffering is deeply unequal. The Levant — already carrying the Arab world's highest baseline poverty rates — is expected to absorb more than 75% of the entire region's poverty increase.

People Pushed Into Poverty (Upper Estimate)

Additional people falling below the poverty line by sub-region

Countries like Lebanon entered this escalation already weakened by years of economic collapse, political dysfunction, and prior conflict. Syria and Iraq carry deep wounds from decades of instability. Jordan and Palestine face chronic resource pressures. For these populations, a five-week military escalation is not merely an economic inconvenience — it is the difference between stability and destitution.

Poverty Impact by Sub-Region

| Sub-Region | Poverty Rate Increase | People Pushed Into Poverty | Share of Regional Total |

|---|---|---|---|

| Levant | +4.45% to +5.15% | 2.85M – 3.29M | Over 75% |

| LDCs (Sudan & Yemen) | +0.15% to +0.60% | 137K – 560K | ~14% |

| North Africa | +0.03% to +0.05% | 59K – 103K | ~3% |

| GCC | Not modelled | Very low baseline | — |

Human Development — A Generation's Progress in Reverse

Beyond the immediate numbers, the UNDP uses the Human Development Index (HDI) — its composite measure of health, education, and living standards — to assess the longer arc of damage.

The findings are grim.

It is worth pausing on the GCC figure. These are among the wealthiest nations in the Arab world — nations with massive sovereign wealth funds, diversified investment portfolios, and strong fiscal buffers. Yet even they face a setback of up to two years of development progress. For the Levant and LDCs, where development gains are hard-won and social safety nets are thin or nonexistent, the damage is generational.

Human Development Index (HDI) Impact

| Sub-Region | HDI Change | Years of Progress Lost |

|---|---|---|

| GCC (Gulf States) | –0.3% to –0.5% | 1.2 – 2.0 years |

| Levant | –0.4% to –0.7% | 0.9 – 1.5 years |

| North Africa | +0.0% to +0.1% | Marginal gain |

| LDCs (Sudan & Yemen) | –0.0% to –0.1% | Small but significant |

The UNDP explicitly flags that in Sudan and Yemen, even tiny HDI declines carry outsized human consequences due to the very low baseline. When you are already near the bottom of the global development ladder, every fraction of a percentage point represents lives.

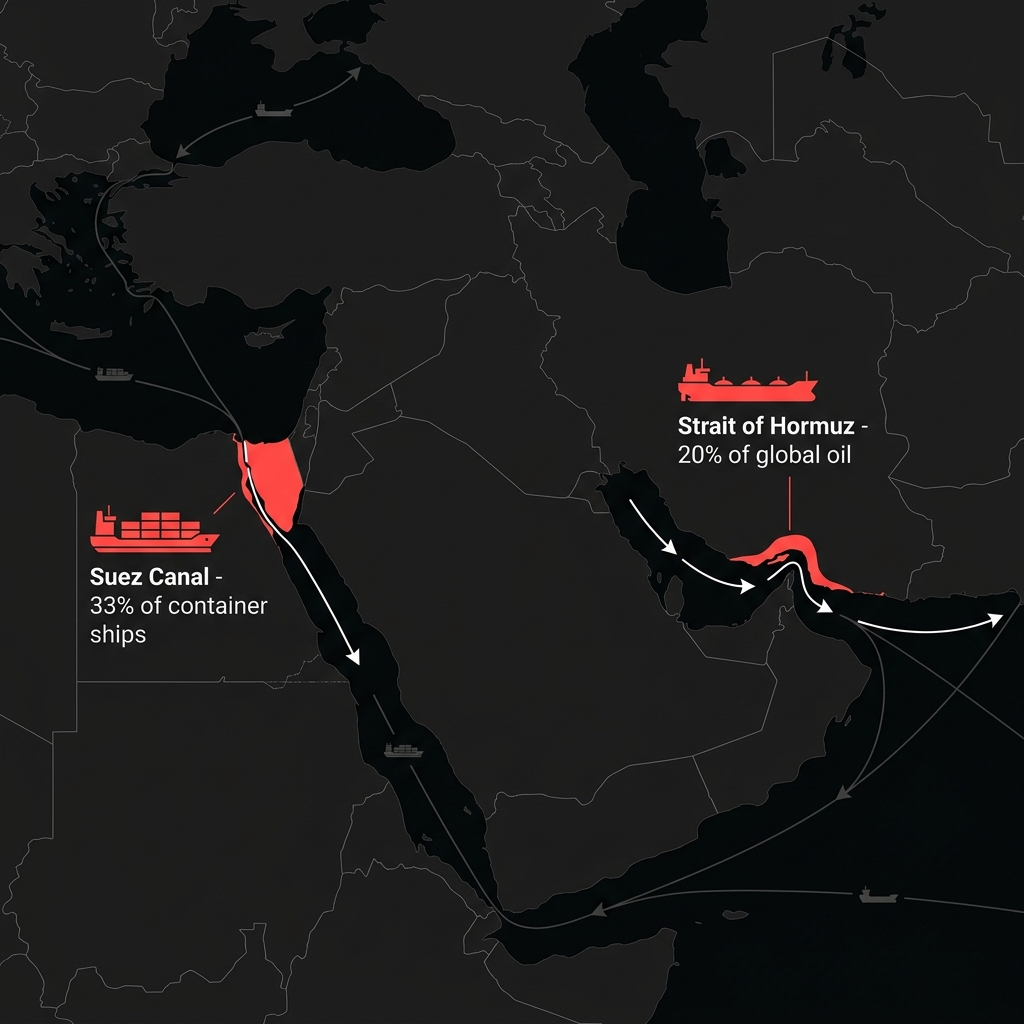

Energy and Trade — The World's Most Dangerous Chokepoints

No analysis of the Middle East's economic impact would be complete without examining the two maritime chokepoints that make this region so strategically critical to the entire global economy.

The Strait of Hormuz

The Strait of Hormuz, located between Iran and Oman, is the single most important oil transit route in the world. Approximately 20% of all global oil exports pass through this 33-kilometre-wide waterway. It is deep enough to accommodate the world's largest oil tankers, and for most Gulf producers, there is no practical alternative route.

Saudi Arabia and the UAE have invested in bypass infrastructure — Saudi Aramco's East-West Pipeline to the Red Sea and the UAE's Fujairah pipeline to the Gulf of Oman — but these operate near full capacity and could only offset roughly 2.6 million barrels per day of disrupted flow in a crisis.

During the current escalation, Iran has effectively closed the Strait to most commercial traffic.

The Suez Canal

The Suez Canal is the world's most important commercial shipping shortcut, connecting the Mediterranean Sea to the Red Sea and providing the fastest maritime route between Europe and Asia. In 2021, roughly a third of all global container ships transited Suez.

That was before the Houthi rebel attacks in Yemen began targeting Red Sea shipping in 2024. By the end of 2024, Suez Canal traffic had already fallen by 42%, forcing shipping companies to reroute around the Cape of Good Hope — adding weeks and thousands of dollars to every voyage.

The knock-on effects are felt in food prices, fuel costs, pharmaceutical supplies, and consumer goods across dozens of countries that rely on efficient sea freight. Egypt, whose economy depends significantly on canal toll revenues and tourism, is among the most directly exposed.

The UNDP and humanitarian agencies are explicit: if both the Strait of Hormuz and the Suez Canal remain severely disrupted simultaneously, food prices will soar, health systems in import-dependent countries will be squeezed, and basic goods will become scarce. The humanitarian and economic consequences would extend far beyond the Middle East.

The Humanitarian Crisis on the Ground

Behind every economic statistic is a human story. UN humanitarian agencies paint a picture of escalating civilian suffering across the region.

Health Systems Under Siege

In Iran alone, the Red Crescent Society has reported damage to 289 health facilities and 600 schools, along with destruction of more than 87,000 civilian residential and commercial units. Hospitals, clinics, and emergency services across Iran, Lebanon, Syria, Gaza, and other conflict-adjacent areas have been struck or rendered inoperable.

In Gaza, the situation remains catastrophic. More than 18,000 patients — including approximately 4,000 children — have no access to specialist medical care. Medical evacuations remain suspended. All border crossings except Kerem Shalom for limited humanitarian supplies remain closed.

Aid Corridors Blocked

The humanitarian fallout from the escalation of violence in the Middle East is increasingly daunting.

Airspace closures have disrupted UN humanitarian flight rotations. Gas flows into Syria have been interrupted. UN humanitarian flights in Yemen have been grounded. The combination of aerial access restrictions and maritime route disruptions is creating an unprecedented pinch point for humanitarian supply chains.

Food Security

In Yemen — already a country facing famine conditions before this escalation — any further disruption to fuel and commodity imports risks immediate price spikes that could tip millions more into acute hunger. The World Food Programme and OCHA have both activated contingency plans across the region, including in Afghanistan, Pakistan, Lebanon, the occupied Palestinian territory, Syria, and Yemen.

What the World Outside the Arab States Is Facing

This is not a regional crisis that stops at the borders of the Arab world.

Global Economic Ripple Effects

| Country / Region | Key Exposure | Projected Impact |

|---|---|---|

| Europe | Major energy importer & trade partner | GDP growth –1pp+ more than forecast |

| Japan | 95% of crude oil from Middle East | Existential energy security threat if Hormuz closes |

| India | Remittances, capital outflows, currency pressure | Rs 20,000 Cr ($2.4B) foreign investor flight in 4 days |

| Egypt | Suez Canal revenues + tourism collapse | IMF-backed reform program at serious risk |

| Global (WTO) | Sustained high energy prices | –0.3% global GDP growth forecast |

Brussels has slipped into a starkly paralysed role as a mere commentator on the geopolitical upheaval on its southern flank.

The Structural Vulnerability Problem

Perhaps the most important and underreported finding in the UNDP report is not any single statistic — it is the underlying diagnosis of why a five-week conflict can cause this much damage.

The Arab States region carries deep structural vulnerabilities that amplify external shocks:

1. Hydrocarbon Dependence. Despite decades of talk about diversification, many Arab economies — particularly in the GCC — remain heavily dependent on oil and gas revenues. When energy markets are disrupted, the entire economic architecture of these states shakes.

2. Trade Concentration. The region's trade routes are heavily concentrated through a small number of maritime corridors. There is limited redundancy. When Hormuz or Suez is disrupted, there is no easy alternative.

3. Underdeveloped Social Protection. Across much of the Levant and the LDCs, social safety nets are thin or non-existent. When jobs disappear and prices rise, households have no buffer. Poverty comes fast.

4. Pre-Existing Fragility. Countries like Lebanon, Syria, Sudan, and Yemen entered this escalation already in crisis. Their institutions are weakened. Their governments have limited fiscal space. Their populations are already overstretched.

5. Regional Interdependence Without Coordinated Resilience. The Arab world is economically interconnected — through trade, remittances, investment flows, and shared energy infrastructure — but lacks robust mechanisms for coordinated crisis response.

This crisis rings alarm bells for countries of the region to fundamentally reevaluate their strategic choices of fiscal, sectoral, and social policies, representing an important turning point in the development trajectory of the region.

What Needs to Happen — The UNDP's Recommendations

The UNDP is direct about what it believes must happen, both immediately and in the longer term.

Immediate Priorities

1. End the Conflict

The UNDP is unambiguous — no sustainable economic or social recovery is possible while active hostilities continue. Every additional day of conflict adds more damage that will take years to repair.

2. Humanitarian Assistance at Scale

Emergency food, medicine, water, shelter, and protection for civilians across conflict-affected zones. This means keeping aid corridors open, funding UN emergency response plans, and protecting humanitarian workers.

3. Social Protection for the Vulnerable

Targeted cash transfers, employment support, and emergency safety nets for the millions of households whose livelihoods have been disrupted. The Levant and LDC populations are priority.

4. Early Recovery Investment

The UNDP is already initiating early recovery activities in conflict-affected areas — restoration of community electricity and water services, support for micro and small enterprises, and livelihood recovery programs.

Longer-Term Structural Reforms

5. Economic Diversification

Arab states — particularly those in the GCC — must accelerate the transition away from hydrocarbon dependency. Expanding manufacturing, services, technology, and renewable energy sectors would reduce vulnerability to energy market shocks.

6. Secure and Diversified Trade Routes

Investment in alternative logistics networks, expanded pipeline infrastructure, and regional trade agreements that reduce concentration risk in key maritime chokepoints.

7. Strengthen Regional Cooperation

The Arab world's political fragmentation reduces its ability to respond collectively to shared economic crises. Stronger regional institutions, coordinated fiscal policies, and mutual economic support mechanisms would make the entire region more resilient.

8. Build Social Protection Systems

Countries in the Levant and LDC grouping need permanent, adequately funded social protection infrastructure — not just emergency responses during crises.

Conclusion

The UNDP's March 2026 assessment is more than an economic report. It is a document about the cost of instability — not just in dollars and jobs, but in human lives, in children who won't receive education, in patients who won't receive care, in workers who will return home to tell their families there is no income this month.

The numbers tell one part of the story: $120 to $194 billion in GDP losses. 1.61 to 3.64 million jobs gone. 3.05 to 3.96 million people pushed into poverty. Half a year to a full year of human development progress erased. And all of this from a conflict that, so far, remains geographically contained.

The other part of the story is the warning embedded within these figures. The Arab States region — home to more than 400 million people — has built its economies and societies on foundations that are more fragile than their oil revenues and gleaming skylines suggest. Two chokepoints control the flow of energy to the world. One region's political instability can erase a year of global GDP growth. One month of war can undo a year of economic progress.

The UNDP's call to action is clear: end the conflict, protect the vulnerable, diversify the economies, and build the regional architecture needed to make the Arab world genuinely resilient to the shocks that — if history is any guide — will continue to come.

The world is watching. The question is whether the right lessons will finally be learned.

📋 Fact Box: Key Numbers at a Glance

GDP LOSSES

- Arab Region Total: $120B – $194B (–3.7% to –6.0%)

- GCC: $103B – $168B (–5.2% to –8.5%)

- Levant: $17.3B – $28.9B (–5.2% to –8.7%)

- North Africa: Marginal gain (0.0% to +0.4%)

- LDCs: $70M – $320M (–0.1% to –0.5%)

EMPLOYMENT

- Jobs Lost (Region): 1.61 – 3.64 million

- GCC Jobs Lost: 1.17 – 3.11 million

- Levant Jobs Lost: ~320,000

- North Africa: ~60,000 · LDCs: 50K – 200K

POVERTY

- Total Pushed Into Poverty: 3.05 – 3.96 million

- Levant: 2.85 – 3.29M (+4.45% to +5.15%)

- LDCs: 137K – 560K · North Africa: 59K – 103K

DEVELOPMENT & TRADE

- HDI Setback (Region): 0.5 – 1.0 year erased

- GCC HDI: 1.2 – 2.0 years lost · Levant: 0.9 – 1.5 years

- Suez Canal Traffic: –42% (2024)

- Hormuz: ~20% of global oil · Japan: ~95% of oil imports from ME

- WTO Warning: –0.3% global GDP · Europe: –1%+ beyond forecast

Sources & References

UNDP — Military Escalation in the Middle East: Economic and Social Implications for the Arab States Region (March 2026) UNDP Press Release — Escalation Reverses More Than a Year of Economic Growth (March 2026) UN OCHA — Statement by Tom Fletcher, Under-Secretary-General for Humanitarian Affairs (March 3, 2026) International Crisis Group — Conflict and Consequences: The Global Impact of the New Middle East War (March 2026) World Trade Organization — Global Trade Outlook, 2026 TRENDS Research & Advisory — Oil, Missiles and Power: The Geopolitics of the Iran-Israel Conflict (2025) Wilson Center — Political Swings in the Middle East in 2025 Al Jazeera — One Month of War on Iran Cost Arab Countries Up to $194bn: UNDP (March 2026) Anadolu Agency — UN Development Agency Warns Middle East War Could Slash Regional GDP by Up to $194B (March 2026) European Union Institute for Security Studies — War in the Middle East: What Implications for the EU and the World? (March 2026)This article is part of StoryRendered's ongoing investigative coverage of the Middle East conflict and its global economic consequences. All research is sourced from verified UN and international institutional reports. If you value independent, documented journalism — consider supporting us.